Publication: Next business day after the Last Trading Day

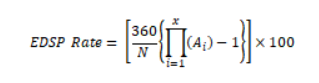

100 minus the EDSP Rate, determined as described below. Based on

ESTR (Euro short-term rate) as calculated by the Benchmark

Administrator each business day, the EDSP Rate represents the

effective rate of interest achieved by reinvesting at ESTR for each

day of the accrual period of the contract. The following formula

shall be applied:

Click

here for EDSP Rate Formula

where:

x = the number of ESTR rates determined in the Accrual Period.

N = the total number of calendar days in the Accrual Period; and

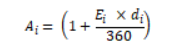

Ai = the overnight return factor in respect of the ith ESTR rate of

the Accrual Period, determined as

Click

here for EDSP Ai Formula

where:

and rounded to eight decimal places, where:

Ei = the ith ESTR rate of the Accrual Period, expressed in such a

way that for a rate of 1% per annum, Ei = 0.01000.

di = the number of days that Ei is applied, such that di represents

the number of calendar days between the day in respect of which the

rate Ei is determined and the next day on which a ESTR rate is

published.

Where the EDSP Rate is not an exact multiple of 0.00001, it will be

rounded to the nearest 0.00001 or, where the EDSP Rate is an exact

uneven multiple of 0.000005, to the nearest lower 0.00001.

For calendar days on which the ESTR rate is not computed (e.g.,

Saturdays, Sundays and bank holidays) the rate shall be the rate

determined on the most recent business day for which a rate was

determined.

{kind=link}

{kind=link}