The NYSE® FANG+™ Index: High Performance at Controlled Risk

The next generation in tech

By Howard L. Simons, President of Rosewood Trading

July 2020

Experienced investors often shy away from market speculation. Normally this is a useful instinct as market history is filled with manias followed by panics and crashes. But what if we could invest in a concentrated but still broad-based index with performance since its 2014 inception exceeding that of common and related investment benchmarks with very controlled levels of risk?

The NYSE FANG+ is such an index. It’s comprised of ten highly liquid stocks representative of the information technology and Internet/media sectors, Facebook®, Apple®, Alphabet®, Amazon.com®, Alibaba®, Netflix®, NVIDIA®, Baidu®, Tesla® and Twitter®. It is an equal-weighted index rebalanced on the March/June/September/December quarterly expiration cycle; a full description of the methodology is available here.

Investment and trading opportunities are created by differences in performance, by risk characteristics and by responses to external factors. The NYSE FANG+ Index is highly suitable for those seeking an outright trading vehicle and for those looking to trade the spread between it and indices such as the S&P 500 and NASDAQ 100.

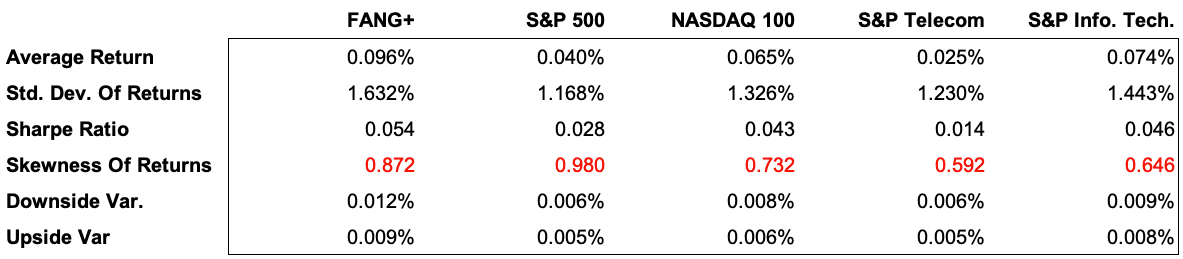

Risk and performance

Let’s look at the performance on a total return basis in U.S. dollars of the NYSE FANG+ Index relative to a set of widely accepted investment benchmarks over the period of September 19, 2014 through June 5, 2020.

Source: ICE

The strong performance of the NYSE FANG+ Index, a period return of 397 percent versus 290 percent for its nearest competitor, the S&P 500 Information Technology Index, might be dismissed as small-sample bias or even as the singular result of strong short-term performances by individual stocks, but closer examination of performance data tell a different story.

Let’s look at standard risk and return measures for this set of indices. As expected from the performance data, the NYSE FANG+ Index has the highest average daily return of 0.096 percent, well above the 0.074 percent registered for the S&P 500 Information Technology Index.

A similar hierarchy applies for the standard deviation of daily returns, 1.632 percent for the NYSE FANG+ Index versus 1.443 percent for the S&P 500 Information Technology Index. However, the Sharpe ratio of 0.054 for the NYSE FANG+ Index versus 0.043 for the S&P 500 Information Technology Index indicates investors were rewarded for assuming this greater variance of returns. Both the downside and upside variance of returns are greater for the NYSE FANG+ Index than for any of the other indices examined, 0.012 and 0.009 percent, respectively.

Surprisingly, the skewness of returns for the NYSE FANG+I Index, while more negative than that for the NASDAQ 100, S&P 500 and Information Technology indices, is less negative than the skewness of returns for the S&P 500 Index. This may be attributable to the NYSE FANG+ Index’ lower exposure to the weak-performing sectors in finance, energy and basic materials prevalent since September 2014.

Risk & Performance Statistics

September 2014 - June 2020

Source: ICE

Now let’s look at a correlation matrix of returns over this period to identify where the strength of similarity between the indices.

Correlation of Returns

September 2014 - June 2020

Source: ICE

The NYSE FANG+ Index is more than just a clone of the NASDAQ 100 or S&P 500 Information Technology indices; its correlations of returns against these two indices, 0.898 and 0.869, respectively, are lower than the correlations of returns for the S&P 500 against those two indices, 0.941 and 0.941, respectively.

External market factors

Performance is affected by multiple intrinsic factors, such as market capitalization and price/book ratio and other value measures. Let’s focus here on some external market factors and see how they relate to each of the stock indices before us. These will include the ICE U.S. Dollar Index® (USDX®), the yield to maturity for two- and ten-year Treasuries (UST-2 and UST-10), a measure of the shape of the U.S.

Treasury yield curve discussed below (FRR), Louisiana Light Sweet crude oil, also discussed below (LLS), the ten-year Treasury Inflation-Protected Securities breakeven rate (BE-10), gold, and the volatility indices calculated by the CBOE for the S&P 500 and NASDAQ 100 indices (VIX and VXN), respectively. The FRR is the annualized rate at which we can lock in borrowing costs for eight years starting two years from now, divided by the ten-year rate itself.

This measure effectively is the tangent of the yield curve and is independent of the ordinal level of interest rates. This is an important consideration as yields and therefore simple yield curve spreads remain compressed. A positively sloped yield curve has an FRR greater than 1.00 while an inverted yield curve has an FRR less than 1.00.

Louisiana Light Sweet (LLS) crude oil at the U.S. Gulf Coast tracks the global benchmark of Dated Brent very closely as they are of similar refining value. The advantage of using this price is it has not been subject to the large expansion of the so-called mid-continent discount in the U.S. and is less affected than Dated Brent both by refining economics in Northwest Europe and by transportation differentials in the Atlantic Basin.

Two measures of statistical relationship are presented below. The first is the R-squared of a linear regression over the sample period; this tells us what percentage of the variance in each stock index can be explained by the external market factor. R-squared levels move between 0.00 for complete randomness to 1.00 for complete determination.

As an aside, we should not expect these R-squared levels to be very high as stock index total returns are affected far more by company-specific and intrinsic factors (alpha) and the general behavior of the stock market itself (beta).

R - Squared of Stock Index Returns Against Selected Markets

September 2014 - June 2020

Source: ICE

The second measure is the partial contribution or degree of association between the market factor and the stock index’ total return series. These can be both positive and negative.

Partial Contribution of Stock Index Returns Against Selected Markets

September 2014 - June 2020

Source: ICE

The NYSE FANG+ Index is less affected by the USDX than are either the S&P 500 or the NASDAQ 100 indices.

While the partial contribution of two-year Treasury yields is similar for the NYSE FANG+ and the S&P 500 indices, the NASDAQ 100 Index is affected much less. The most negative partial contribution for the FRR is for the S&P 500 Index, which has heavy exposure to the financial sector. The breakeven rates of inflation for Treasury Inflation Protected Securities have been a minor factor over this sample period.

However, the opposite relationship obtains for gold.

The partial contribution of LLS to the NYSE FANG+ Index is similar to those for the NASDAQ 100 and S&P 500 Information Technology indices, but is significantly lower than that for the S&P 500 Index. This is unsurprising given the broad market’s inclusion of the energy and financial sectors. As crude oil has been under pressure for most of the sample period, the lower exposure of the NYSE FANG+ Index to it has contributed to its outperformance of the other indices.

Finally, the NYSE FANG+ Index has the strongest exposure of the U.S. indices examined to both the VIX and VXN. This is consistent with the index’ higher standard deviation of returns and greater upside and downside variances. We should put aside the growing question of whether implied volatility is a function of stock index fluctuations or if volatility trading strategies increasingly are influencing the stock indices and simply accept the observed linkage between the NYSE FANG+ Index and the implied volatility measures.

Spread trade relationships

Whether we recognize it consciously at the time, all financial market trades are spreads. At its simplest, the purchase of a stock is a swap of cash’s return for the stock’s return. Spread trades can be classified into categories such as process spreads, like the crack spread in petroleum market, joint product spreads, such as ultra-low sulfur diesel fuel against RBOB gasoline, substation spreads, such as canola against soybeans, and related spreads, such as equity matched-pair and index spreads.

Related spreads involve markets with general economic relationships not inclusive of substitution or joint product attributes. As such, they have no economic bounds or physical process constraints and no mean-reverting tendencies.

Restated, a related index spread can move along in a long-term trending relationship so long as new information comes into the market supportive of the underlying trend. New information can also change the underlying economic value of the asset and produce new prices.

As changes in information can move in one direction persistently and as the risk-acceptance of market participants can rise and fall in herd-like fashion, stock index spreads often exhibit the same autoregressive behavior observed for each index involved. This can be illustrated by mapping the incremental total return of the NYSE FANG+ Index to both the S&P 500 and NASDAQ 100 indices. These incremental returns exhibit persistent trends.

FANG+ Incremental Total Return vs. Nasdaq 100 and S&P 500

Source: ICE

These trends can be traded simply and efficiently by using NYSE FANG+ Index Futures on ICE Futures U.S.® and, for purposes of illustration, E-mini S&P 500 and E-mini NASDAQ 100 futures on the CME Group. A complete description of NYSE FANG+ Index Futures can be found here.

The sample period for the discussion below begins with the launch of these futures on November 8, 2017 and extends through June 5, 2020. As the index futures have the same quarterly expiration cycle, a continuous front-month contract will be used.

First, let’s establish the hedge ratios between the index futures. This can be done by converting the respective futures prices into dollar equivalents by using the contract multipliers of $20 per index point for the NASDAQ 100 E-mini Index Futures and $50 per index point for both the NYSE FANG+ and S&P 500 E-mini Index Futures. The products will be referred to as NYFANGD, SPXD and NDXD. The following regression synopses were obtained:

NYFANGD = 1.003 * NDXD – 13508; r2 = 0.774, D-W = 0.022

NYFANGD = 1.175 * SPXD – 29848; r2 = 0.372, D-W = 0.013

The 1.003 beta for the NDXD indicates we can use a simple 1:1 hedge ratio, while the 1.175 beta for the SPXD indicates we should trade 7 S&P 500 E-mini® futures against 6 NYSE FANG+ Index Futures. The very low Durbin-Watson (D-W) statistics are consistent with the autoregressive nature of stock indices and their strong suitability for long-term spread trading. If we included other independent variables, we could build a superior model and see the D-W move toward the unbiased level of 2.00, but this would be irrelevant to the objectives of investing and trading.

Like all stock index futures, NYSE FANG+ Index Futures offer superior capital use efficiencies. While initial and maintenance margin levels rise and fall with market volatility, exposure to the index can be acquired with a single trade for 22 hours per day at a mid-June 2020 a minimum initial margin level of $20,325.70 and a maintenance margin level of $18,477.90. This compares to an index contract value in the neighborhood of $200,000.

Moreover, the gains and losses on these futures trades are eligible for IRS Section 1256 tax treatment (60 percent long-term / 40 percent short-term capital gains). As always, consult with a tax professional for full understanding of tax treatment, including hedge accounting and the constructive sale rule.

No single investment exposure or trading strategy works permanently. However at present, the NYSE FANG+ Index offers superior performance characteristics without the assumption of outlandish risk, different responses to external market factors and long-term trending spread opportunities against other broad-based stock indices. What more can we ask?

Howard L. Simons is president of Rosewood Trading, Inc. (AKA Simons Research). He has served as an economist, oil trader, trading systems designer, director of research, consultant to exchanges, broker-dealers, private banks and hedge funds and professor of finance. Simons writes on macroeconomic and financial market topics including fixed-income, commodities, currencies, derivatives and equity markets.

For further information about the NYSE FANG+ Index, visit this page. The NYSE FANG+™ Index (“Index”) is a trademark of ICE Data Indices, LLC or its affiliates ("ICE Data") and has been licensed for use in connection with the NYSE FANG+ Index Futures and NYSE FANG+ Index Options. The NYSE FANG+ Index Futures and the NYSE FANG+ Index Options are not sponsored, endorsed, sold or promoted by ICE Data. ICE Data makes no representations or warranties (i) regarding the advisability of investing in securities or futures contracts or options, or (ii) that any such investment based upon the performance of the NYSE FANG+ Index particularly, or the ability of the NYSE FANG+ Index will track general stock market performance.

The information and materials contained in this document - including text, graphics, links or other items - are provided "as is" and "as available." ICE and its subsidiaries do not warrant the accuracy, adequacy or completeness of this information and materials and expressly disclaims liability for errors or omissions in this information and materials. This document is provided for information purposes only and in no way constitutes investment advice or a solicitation to purchase investments or market data or otherwise engage in any investment activity. No warranty of any kind, implied, express or statutory, is given in conjunction with the information and materials. The information in this document is liable to change and ICE undertakes no duty to update such information. You should not rely on any information contained in this document without first checking that it is correct and up to date.