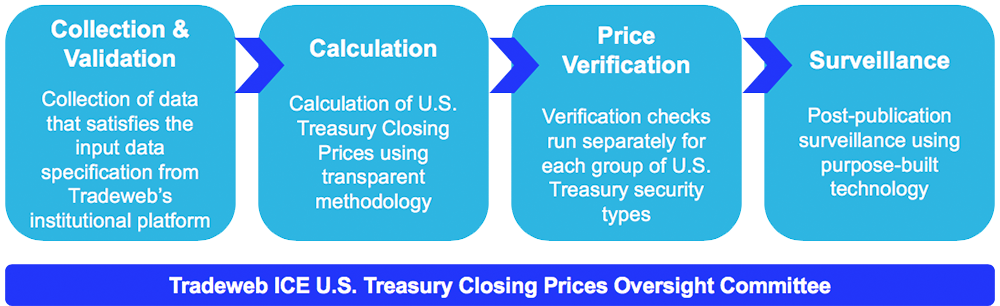

Each Tradeweb ICE U.S. Treasury Closing Price for a U.S. Treasury Security is calculated in accordance with the Methodology, The calculation uses bid and offer quotes for the relevant security from dealers on Tradeweb’s institutional platform. The quotes are subject to certain special cases, as described in the Methodology. On the Tradeweb Platform, the quotes are attributable to specific dealers and are executable by the receiving institutional client, subject to the dealer accepting the trade.

Key Features of the Calculation

Multiple, Random Snapshots

Tradeweb uses fifteen, randomised, 2-second market snapshots of bid and offer quotes for a given U.S. Treasury Security from dealers on the Tradeweb’s institutional platform taken during a thirty-second collection window immediately before 15:00 and 16:00 ET. This enhances the benchmark’s robustness and reliability by protecting against attempted manipulation and temporary aberrations in the underlying market.

Outlier Exclusion

To protect against unrepresentative dealer quotes within a market snapshot influencing the benchmark, dealer mid-prices that are more than one standard deviation from the mean may be excluded from the calculation.

Random Dealer Quote Removal

To protect against the possibility of predicting the impact that a particular quote (or quotes) may have on the benchmark calculation, a number of dealer mid-prices may be randomly eliminated from the calculation.

Special Cases

There are certain special cases where the published price for a U.S. Treasury Security is not derived using bid and offer quotes from Tradeweb’s institutional platform. For example, U.S. Treasury Securities that have fewer than 3 days to maturity are priced at par, and STRIPS with fewer than 7 market snapshots with at least 4 quoting dealers are priced using a zero-coupon curve.

Multiple, Random Snapshots

Tradeweb uses fifteen, randomised, 2-second market snapshots of bid and offer quotes for a given U.S. Treasury Security from dealers on the Tradeweb’s institutional platform taken during a thirty-second collection window immediately before 15:00 and 16:00 ET. This enhances the benchmark’s robustness and reliability by protecting against attempted manipulation and temporary aberrations in the underlying market.

Outlier Exclusion

To protect against unrepresentative dealer quotes within a market snapshot influencing the benchmark, dealer mid-prices that are more than one standard deviation from the mean may be excluded from the calculation.

Random Dealer Quote Removal

To protect against the possibility of predicting the impact that a particular quote (or quotes) may have on the benchmark calculation, a number of dealer mid-prices may be randomly eliminated from the calculation.

Special Cases

There are certain special cases where the published price for a U.S. Treasury Security is not derived using bid and offer quotes from Tradeweb’s institutional platform. For example, U.S. Treasury Securities that have fewer than 3 days to maturity are priced at par, and STRIPS with fewer than 7 market snapshots with at least 4 quoting dealers are priced using a zero-coupon curve.

Please see the Documentation section below for the full Calculation Methodology.