Managing U.S. dollar risk in uncertain times

The U.S. Dollar Index® (USDX) rallied strongly in April after the demand for the U.S. Dollar persisted. The USDX closed the month with a gain of 1.77% at 106.10 to mark the fourth consecutive bullish month.

- Nonfarm Payrolls recorded an unexpected rise after 303,000 new jobs were added in March, later revised to 315,000, surpassing the expected 200,000 and above the downwardly revised February numbers of 270,000. Following this news the USDX closed the day with a modest gain of 0.06% at 104.07.

- Core Inflation, excluding food and energy, steadied at the near three-year low at 3.8% for the period 12-month ending March, slightly above the market expectations of 3.7%. The Consumer Price Index (CPI) data released surprised the markets after it ticked higher than expected to 3.5% for the period 12-month ending March from 3.2% the prior month. The USDX closed the day with a gain of 1.10% at 105.03.

- The Federal Open Market Committee (FOMC) released the minutes from the meeting held on March 20th which confirmed that all participants agreed to maintain the federal funds rate within the range of 5.25% - 5.50%, seeing it as supportive in returning inflation to 2%.

Insights provided by

Macro Commentary

U.S. Dollar Index® Focus

SYMBOL: DX

High impact events per day

| 10 | Michigan Consumer Sentiment Index |

| 14 | Producer Price Index |

| 15 | Consumer Price Index & Retail Sales |

| 22 | FOMC Minutes |

| 23 | S&P Global Manufacturing PMI (PREL) |

| 24 | S&P Global Services PMI (PREL) |

| 30 | Gross Domestic Product (GDP) Annualized Q1 (PREL) |

| 31 | Core Personal Consumption Expenditures - Price Index |

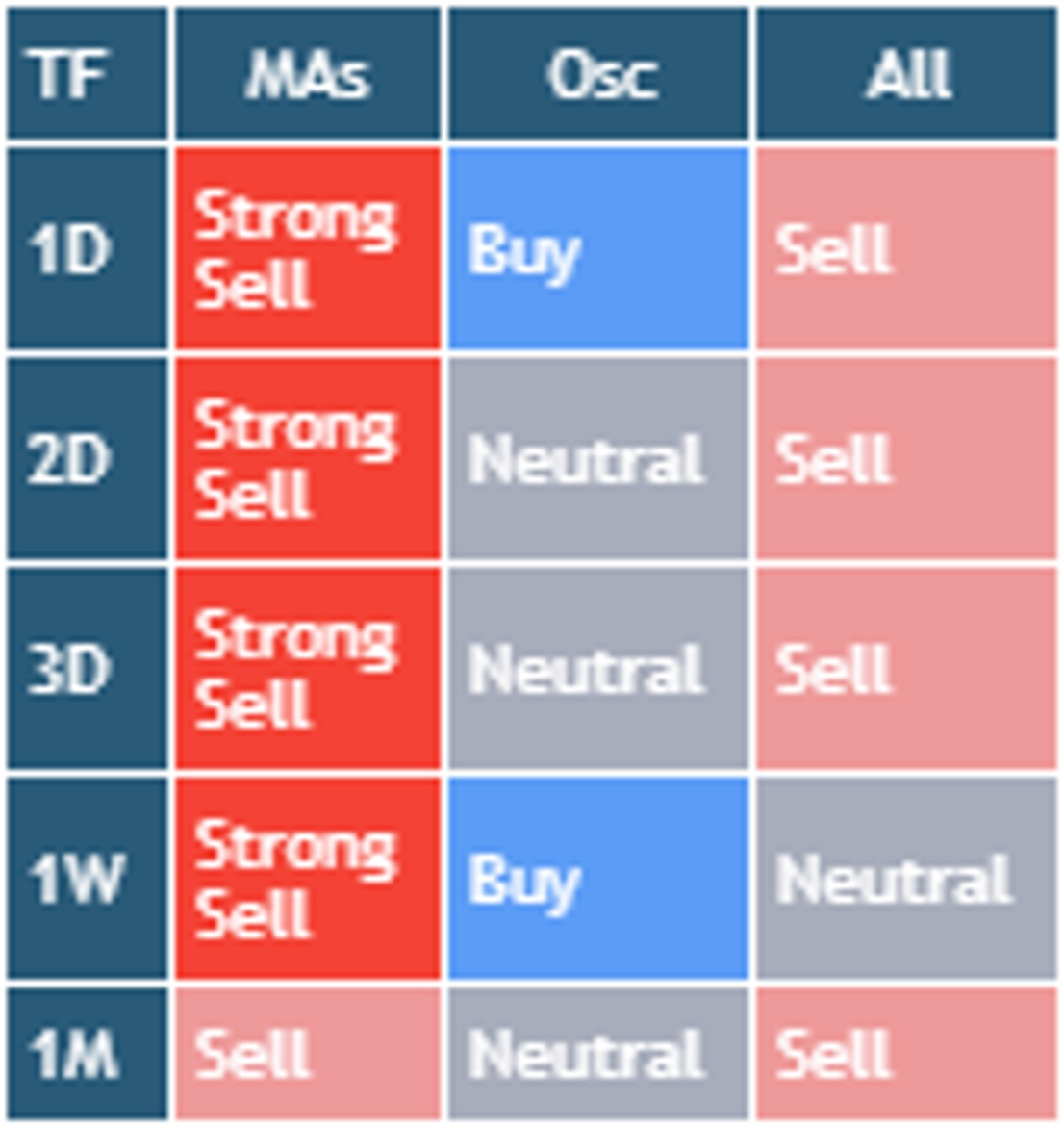

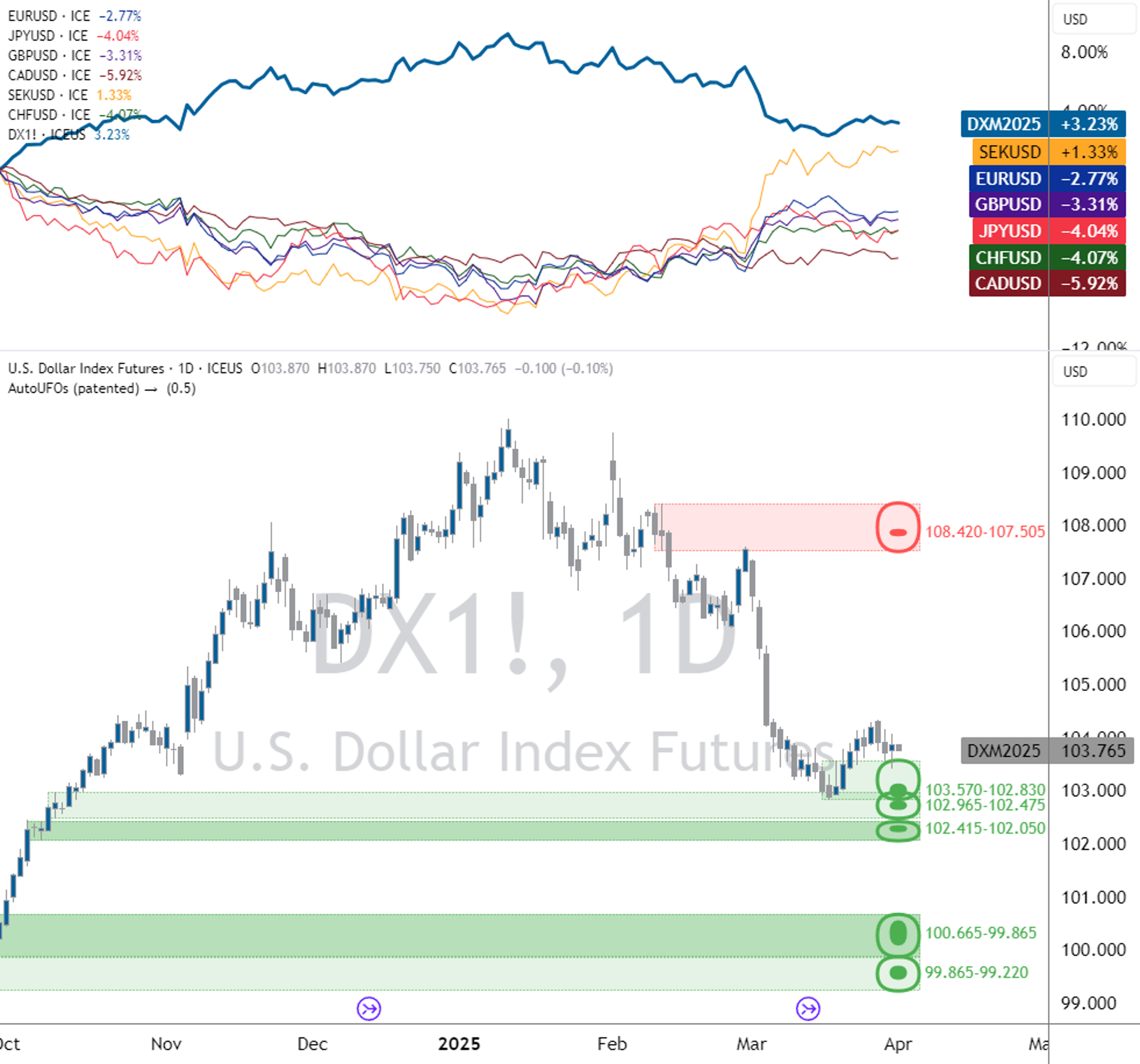

Weighting: EUR 57.6% / JPY 13.6% / GBP 11.9% / CAD 9.1% / SEK 4.2% & CHF 3.6% | Source: TradingView | Conditions Table: using daily SMA (10, 20, 30,50, 100, 200), EMA (10, 20, 30,50, 100, 200), Ichimoku Cloud (9, 26, 52), VWMA (20), HullMA (9), RSI (14), Stochastic (14, 3, 3), CCI (20), ADX (14, 14), Awesome Oscillator, Momentum (10), MACD (12, 26, 9), Stochastic RSI (3, 3, 14, 14), Williams %R (14), Bulls and Bears Power and Ultimate Oscillator (7,14,28) | Support & Resistance Levels: using AutoUFOs® (0.5) applied to a daily timeframe (plotted as dotted lines that represent relevant support and resistance price zones colored as follows: red = resistance levels & green = support levels)

The month of April began on a bullish note for the U.S. Dollar Index® (USDX) after the release of better-than-expected ISM Manufacturing PMI data for March. The market closed at 104.76, within an area of daily resistance between 104.66 and 104.98, recording a gain of 0.49%. However, the following day, the U.S. Dollar Index® struggled to maintain the upside momentum as the bears returned, and the demand for the U.S. Dollar weakened. The U.S. Dollar Index® dropped from the resistance area slightly, closing at 104.56 with a loss of 0.17%. The bearish momentum extended into trading on April 3rd, despite the release of better-than-expected ADP Employment Change data, which recorded 184,000 new private sector jobs (later revised to 208,000) against the prior month's upwardly revised 155,000. This positive data provided a temporary lift for the U.S. Dollar Index®. However, the demand for the U.S. Dollar weakened shortly after, exacerbated by worse-than-expected ISM Services PMI data, which missed both the market forecast and the prior month, falling to 51.40, down 2.28%. Later that day, Fed Chair Jerome Powell held a speech and reiterated the Fed's stance on interest rates. Powell shared that the Fed would take its time before reducing interest rates, as inflation still exceeded the 2% target despite the progress made. He implied that rates might remain elevated for longer, although incoming data would guide the Fed's decisions on a "meeting by meeting" basis. The U.S. Dollar Index® closed the day at 104.00, recording the greatest daily loss for the month at 0.51%. The first week of April trading concluded with the release of the Nonfarm Payrolls report for March. The data revealed an unexpected surge in job creation, with 303,000 new jobs added, surpassing the expected 200,000 and exceeding the downwardly revised February number of 270,000. Following this robust employment data, the U.S. Dollar Index® rallied to a high of 104.46 during the trading session. However, the market ultimately closed the day with a modest gain of 0.06%, at 104.07. The U.S. Dollar Index® closed the first week of April with a loss of 0.17%.

On April 8th, the week began with a fall in demand for the U.S. Dollar after it reached a high of 104.21 where it struggled, closing just below the daily 20 EMA with a loss of 0.15%. On April 9th, the bears drove the market lower, but the index found support at the midpoint of the daily Bollinger Bands. After hitting a low of 103.98, demand returned, and the U.S. Dollar Index® closed with a modest gain of 0.05%. On April 10th, the demand for the U.S. Dollar persisted as the market retested the midpoint of the Bollinger Bands and took a bounce. The momentum gathered further after the release of Core Inflation data for the 12-month period ending March. While the Core Inflation figure, excluding food and energy, remained steady at 3.8%, it missed expectations. However, the Consumer Price Index (CPI) for the same period showed an uptick, with annual inflation for all items recording a rate of 3.5%, higher than the previous 3.2%. Adding to the bullish sentiment, the FOMC minutes released on April 10th revealed that all participants agreed to hold interest rates steady. The minutes highlighted that while the U.S. economy was expanding, it was at a steady pace, slower than the prior quarter. Notably, the minutes expressed a positive outlook on the labor market, which remained strong with robust payroll growth and low unemployment. Fueled by these factors, the U.S. Dollar Index® surged through the daily resistance area, breaching the upper boundary of the daily Bollinger Bands, and closed at 105.03 with a substantial gain of 1.10%, the largest daily gain of the month. On April 11th, the Core Producer Price Index, excluding food and energy, surprised the markets by increasing to 2.4%, slightly above expectations and the prior month's upwardly revised figures. The U.S. Dollar Index® closed at 105.06, up 0.05%, after pulling back from a high of 105.31. Michigan Consumer Sentiment Index Preliminary data announced on April 12th fell short of expectations, although this had little impact on the U.S. Dollar Index® which closed the day up 0.73% at 105.83 as it continued to hug the upper boundary of the daily Bollinger Bands, ending the week with a gain of 1.70%.

The week began positively on April 15th as Retail Sales for March rose 0.7%, beating expectations although lower than February’s upwardly revised figure of 0.9%. Nonetheless the demand for the U.S. Dollar increased and the U.S. Dollar Index® closed the day with a 0.16% gain at 106.00. The bullish momentum continued until the U.S. Dollar Index® reached a weekly and monthly resistance area prompting a pullback on April 17th closing down 0.37%. April 18th saw a return of the bulls as the safe-haven U.S. Dollar attracted inflows, lifting the index 0.18%. However, the week ended on a bearish note on Friday, though the U.S. Dollar Index® still managed a 0.15% weekly gain. The positive Retail Sales data initially boosted the index, while resistance levels and profit-taking activities led to consolidation later in the week.

On April 22nd, the U.S. Dollar Index® pushed back into the resistance area, although it struggled to gain significant ground. On April 23rd, the S&P Preliminary Global Services PMI data showed an unexpected decline in growth to 50.9, falling short of forecasts and the prior release. Additionally, the S&P Preliminary Global Manufacturing PMI data also announced an unexpected fall in manufacturing activity, dropping to 49.9, falling short of forecasts and the prior release of 51.9. The U.S. Dollar Index® weakened on this news to close with a loss of 0.43%. While there was some respite the following day as demand increased, this was short-lived as bearish sentiment returned on April 25th. The release of the GDP Annualized Q1 report data pointed to a fall in anticipated growth to 1.6%, significantly lower than initial forecasts of 2.5% and 3.4% gain in Q4. Consequently the U.S. Dollar Index® closed the day with a loss of 0.21%. However, the demand for the U.S. Dollar returned on Friday after the U.S. Dollar Index® found support at the daily 20 EMA to close the day up 0.33% and end the week at 105.80 with a modest loss of 0.08%.

On Monday April 29th the U.S. Dollar Index® traded lower to record a loss of 0.41% although the U.S. Dollar bulls regained control on the last trading day of the month. The market found support at the daily 20 EMA and took a bounce closing the day with a gain of 0.51%. The U.S. Dollar Index® closed the month at 106.10 with a gain of 1.77%. This marked the fourth consecutive bullish monthly close for the U.S. Dollar Index® in 2024, highlighting the sustained strength of the U.S. Dollar throughout the year's first four months.

The U.S. Dollar Index® was in an uptrend on the daily timeframe using the daily SMA (10 and 20) and daily EMA (20, 30 and 50). The U.S. Dollar Index® was also in an uptrend on the weekly timeframe, based on the weekly SMA (10 and 20) and weekly EMA (10, 20 and 30).

Source: ICE Connect

USDX® Performance

Spot Rates | TICKER | 1-Apr-24 | 30-Apr-24 | Monthly Change* |

|---|---|---|---|---|

| USD/EUR | EUR A0-FX | 1.07428 | 1.06649 | -0.730% |

| JPY/USD | JPY A0-FX | 151.619 | 157.706 | -3.860% |

| USD/GBP | GBP A0-FX | 1.2554 | 1.2494 | -0.480% |

| CAD/USD | CAD A0-FX | 1.35685 | 1.37747 | -1.497% |

| SEK/USD | SEK A0-FX | 10.80457 | 11.01915 | -1.947% |

| CHF/USD | CHF A0-FX | 0.9041 | 0.91845 | -1.562% |

| US Dollar Index | DX A0 | 105.019 | 106.221 | 1.132% |

| Front Month | Ticker | 1-Apr-24 | 30-Apr-24 | Monthly Change |

|---|---|---|---|---|

| Mini USDX | SDX-ICS | 104.764 | 104.269 | 1.259% |

OTHER CONTRACTS | TICKER | 1-Apr-24 | 30-Apr-24 | Monthly Change |

|---|---|---|---|---|

| Brent Crude | BM-ICS | 87.42 | 86.33 | -1.263% |

| MSCI World Index | MWL | 3456.6 | 3316.1 | -4.237% |

| MSCI Emerging Markets Index | MME | 1050.9 | 1042 | -0.854% |

Mini US Dollar/Offshore Renminbi | CHM-ICS | 7.2492 | 7.249 | 0.003% |

Source: ICE Connect

Restrictions on Distribution

The distribution of this document and the offering of any products, investments or strategies mentioned in it may be restricted by law in certain jurisdictions. None of ICE Futures Singapore, Intercontinental Exchange Inc. nor any of their affiliates (collectively, “ICE”) represent that this document may be lawfully distributed, or that any product, investment, or strategy described in it may be lawfully offered in compliance with any applicable laws or requirements in any such jurisdiction.

Disclosure Section

This document does not provide individually tailored financial or investment advice, and no part of this document should be construed as doing so. This document has been prepared without regard to the individual financial or other circumstances and objectives of persons who receive it. Investors and users should independently evaluate particular products, investments, and strategies and are encouraged to seek the advice of a financial advisor. The appropriateness of a particular product, investment or strategy will depend on a user or investor's individual circumstances and objectives. The products, investments or strategies discussed in this document may not be suitable for all users and investors, and certain users or investors may not be eligible to purchase or participate in some or all of them.

ICE Futures Singapore does not provide financial, investment, legal or tax advice and is not in the business of doing so. Each user or investor should always consult a financial, investment, legal or tax advisor for information concerning its individual situation and to learn about any potential financial, investment, legal, tax or other implications that may result from any product, investment or strategy described in this document.

In particular, any opinion contained in this document (including an indication of any “sell”, “neutral” or “buy” condition) is generic and not a recommendation to take (or omit to take) any action in relation to any product, investment or strategy.

Key Information Documents for certain products covered by the EU Packaged Retail and Insurance-based Investment Products Regulation can be accessed on the relevant exchange website under the heading “Key information Documents (KIDS)”.

© 2024 Intercontinental Exchange, Inc. The information and materials contained in this document - including text, graphics, links or other items - are provided for general information only on an "as is" and "as available" basis. Although this document is issued in good faith, no representation, warranty or guarantee, whether express or implied, is or will be made in respect of the information contained herein. ICE excludes all liability arising from or in relation to the accuracy, adequacy, completeness, fitness or timeliness of the information provided and assumes no duty whatsoever. The information in this document is liable to change, and ICE undertakes no duty to update such information. You should not rely on any information contained in this document without first checking that it is correct and up to date. No information set out or referred to in this document shall form the basis of any contract. The content of this document is proprietary to ICE in every respect and is protected by copyright. No part of this material may be copied, photocopied or duplicated in any form by any means or redistributed without the prior written consent of ICE. All third-party trademarks are owned by their respective owners and are used with permission.

Trademarks of ICE and/or its affiliates include Intercontinental Exchange, ICE, ICE block design, NYSE, and New York Stock Exchange. Information regarding additional trademarks and intellectual property rights of Intercontinental Exchange, Inc. and/or its affiliates is located at www.intercontinentalexchange.com/terms-of-use