Exchange traded funds in volatile markets

Understanding the disconnect between price & net asset value

The ETF industry has blown away the growth expectations of its creators in the 1990s. While equities were the initial beneficiaries of investor appetite, bond ETF assets have surged since the 2008 financial crisis. Now bond ETFs - which give broad exposure to fixed income via a single exchange listed instrument - have highlighted challenges within the bond market structure.

Here, we examine characteristics of bond ETFs that help to explain the magnitude of recently observed gaps between the net asset values (NAVs) and prices of bond ETF shares. This phenomenon can be summarized by examining the structure of fixed income markets - fragmented, lacking centralized price discovery, and featuring a wide spectrum of liquidity. By contrast, equity markets have centralized venues, fast price discovery, and are generally more liquid. We believe that investors in bond ETFs can draw reassurance from a better understanding of these factors, and that the rise of electronic trading may offer long-term solutions.

Advantages of ETFs

For investors, the benefits of ETFs include immediate exposure to a broad range of securities traditionally reserved for institutions. Additionally, ETFs have lower transaction costs, good intraday liquidity due to being listed and continuously quoted, and offer tax advantages versus buying a portfolio of individual securities.

These benefits are particularly striking for retail investors who wish to access fixed income, given the complexity of the ~$45 trillion US debt market. If an individual wants exposure to the US bond market, they’d need to sift through ~40,000 corporate bonds, ~1 million municipal bonds and ~10,000 government agency bonds to construct a portfolio. This makes security selection time-consuming and expensive - and requires analysis of bond characteristics such as issuer, sectors, ratings, maturity, coupon, embedded options, seniority and more.

In addition, bonds currently have no central location for price discovery, as they primarily do not trade on exchanges like equities. Instead they trade “over the counter” (OTC) between two parties. This means transparent price discovery is limited and bonds aren’t frequently quoted or traded — just 5-10% of corporate bond issues and less than 1% of municipal bond issues trade on any given day. By contrast, bond ETFs provide a mechanism for investors to easily access bonds within a structure that gives them liquidity similar to equities.

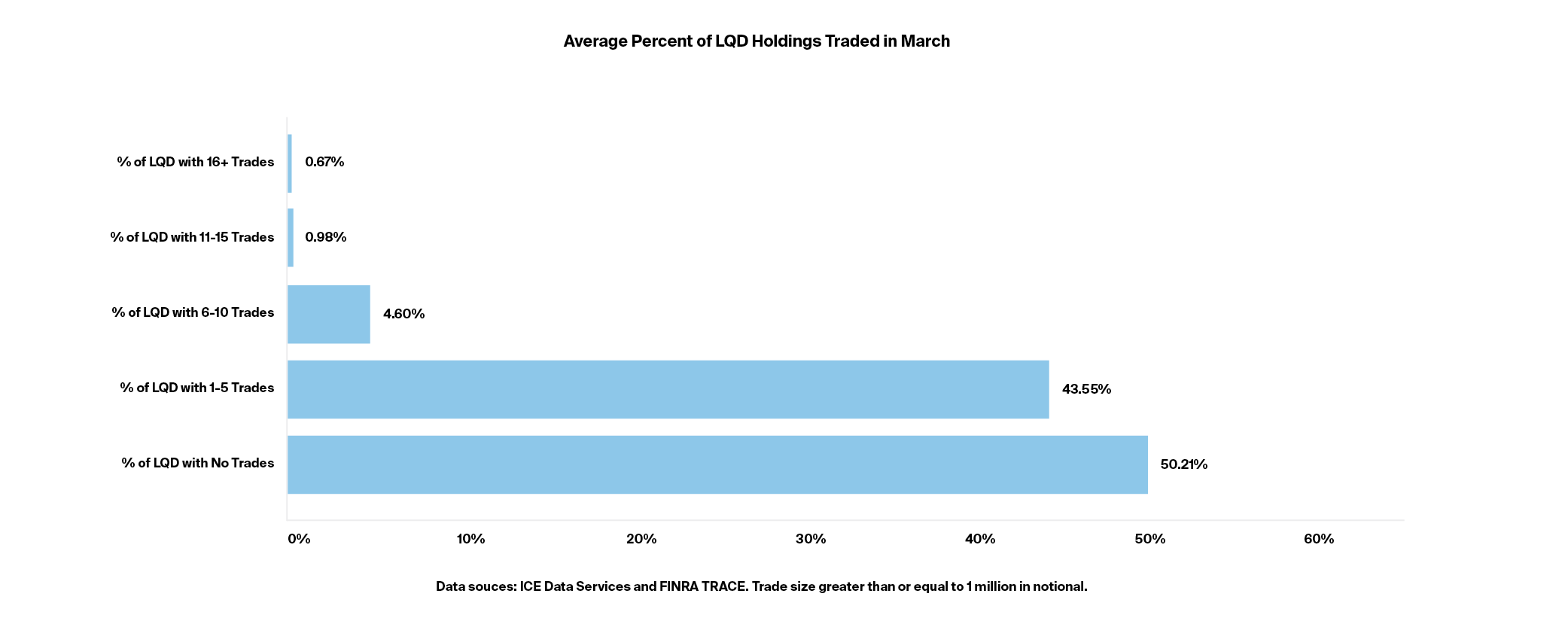

To illustrate the contrast between the liquidity of an ETF and its underlying assets, let’s examine the trading frequency of bonds held by LQD for trades greater than 1 million in notional size. Below, you can see ~40% of the bonds in LQD traded on average 1-5 times per day during March. During the same period, the LQD ETF traded thousands of times per day on the exchange.

Average percent of LQD holdings traded in March

Premium/Discount to Net Asset Value

In volatile markets, bond ETFs tend to be more reactive to market events than changes in their underlying bond prices. It’s this disconnect that causes the gap between the price of bond ETF shares and NAV.

When the price of an ETF share trades above its NAV, this is referred to as a “premium” and when the ETF price trades below its NAV, it’s called a “discount”.

This disconnect is possible as the ETF share price and its underlying assets are not directly tied. Instead, the ETF share price is based on the dynamics of buyers and sellers, while the NAV is a calculation based on all the securities in the underlying portfolio.

Yet there are powerful forces that keeps the ETF price and the NAV close together. Authorized participants (APs) — mostly large dealers and some asset managers - can exchange ETF shares for a pro rata share of the ETF’s underlying securities from the ETF Issuer or vice-versa. This incentive generally keeps ETF prices close to the NAV. For example, if an ETF is trading above the NAV, an AP can buy a representative basket of securities underlying the ETF and offer them to the ETF issuer in exchange for ETF shares. They can then sell the ETF shares in the secondary market for a profit.

This arbitrage opportunity differs starkly for equity and fixed income ETFs. Since equities can trade on exchanges and have actively quoted bids and offers, the process for an AP to transact a basket of stocks can happen almost instantaneously. But because fixed income securities are primarily traded over the counter and often don’t have actively quoted bids and offers, buying or selling bonds can take much longer, especially when there is elevated execution uncertainty during volatile markets. When the arbitrage opportunity for fixed income is slower, it would be fair to expect swings of discounts and premium to be larger and more prolonged.

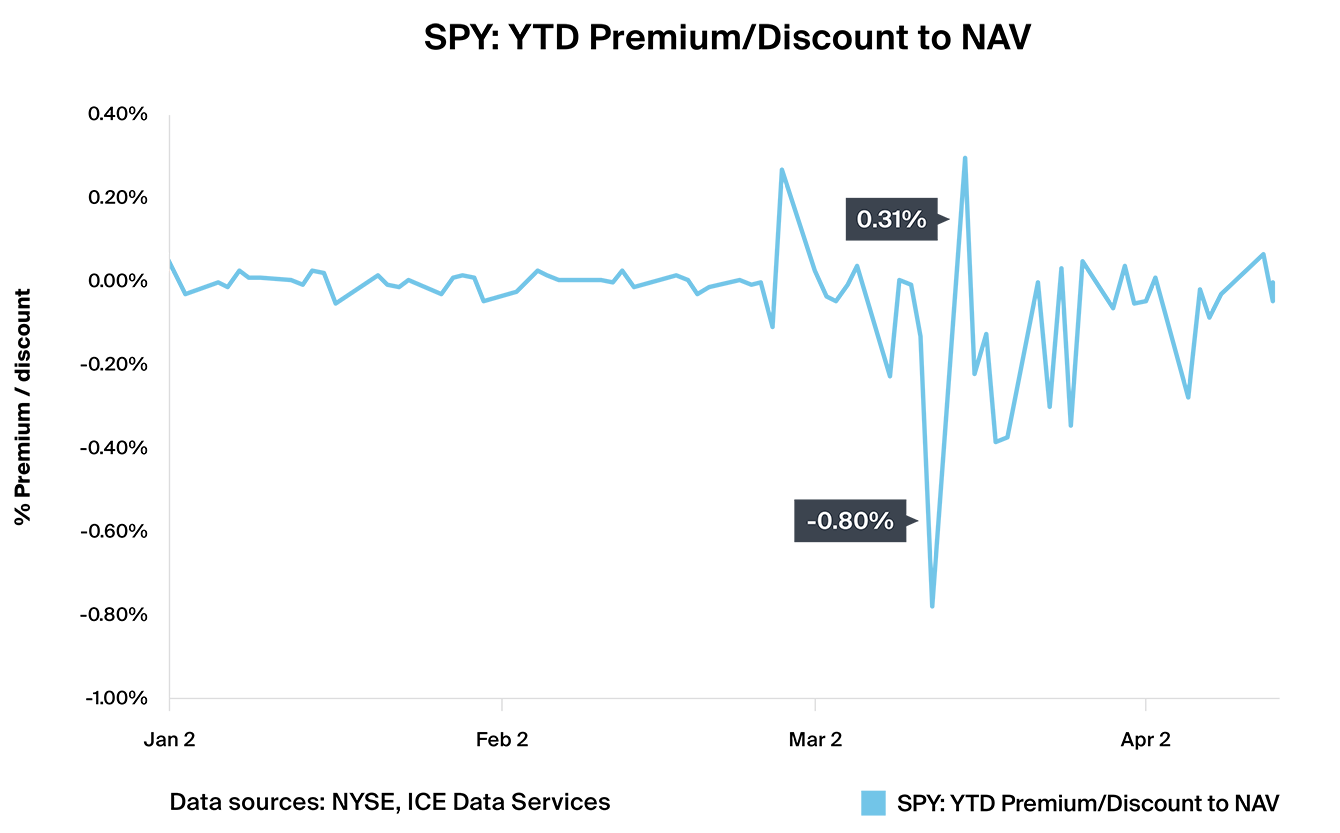

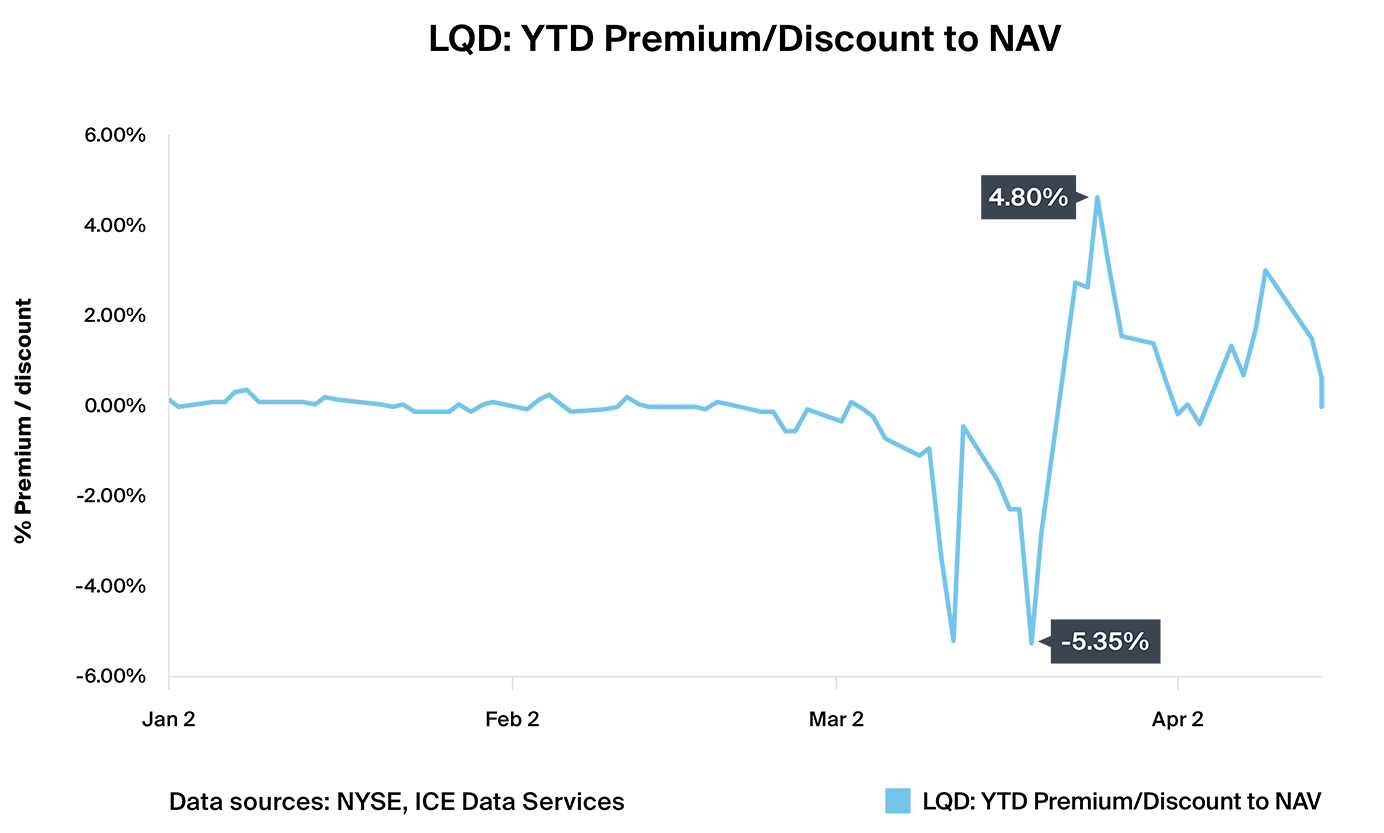

To illustrate this, consider the difference in an equity ETF versus a fixed income ETF — an S&P/500 equity ETF (SPY) vs an Investment Grade Corporate bond ETF (LQD) in 2020.

SPY: YTD Premium/Discount to NAV

LQD: YTD Premium/Discount to NAV

Above, the magnitude of premium/discount of the equity ETF is just -0.80% versus -5.35% for the LQD Investment Grade Corporate bond ETF. In addition, the premium/discount is corrected in about a day for the equity ETF but takes multiple days for the bond ETF. This suggests the liquidity profile difference between equities and corporate bonds can lead to a higher potential premium or discount to NAV.

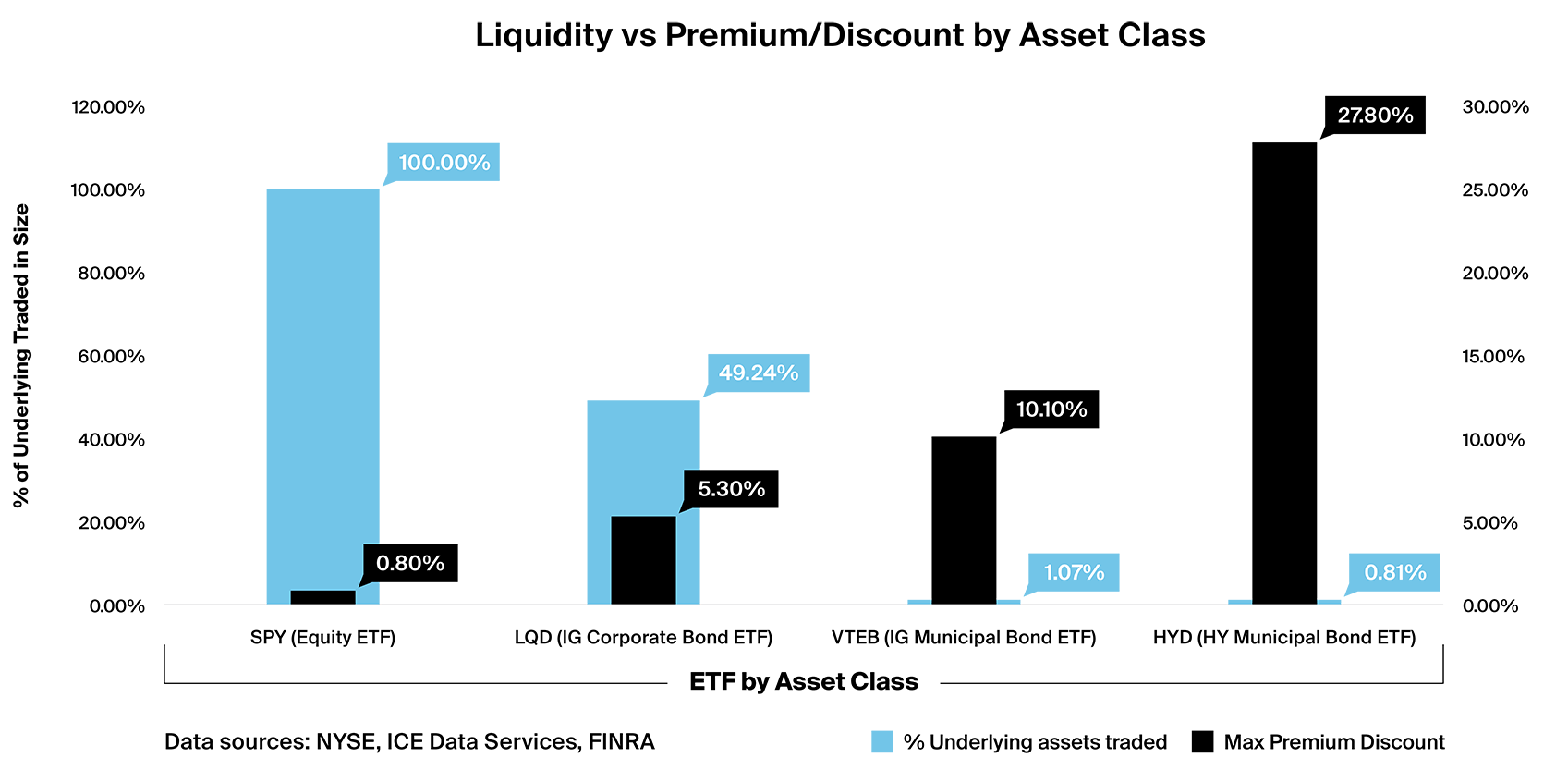

This is further supported by comparing fixed income ETFs from different asset classes with varying liquidity. Below, we show the inverse relationship between the premium/discount of an ETF to the liquidity of its assets on days in March 2020 that had the largest differences to NAV. The more liquid the underlying asset, the less pronounced the premium/discount. The less liquid the underlying asset, the more pronounced it is.

Liquidity vs Premium/Discount by Asset Class

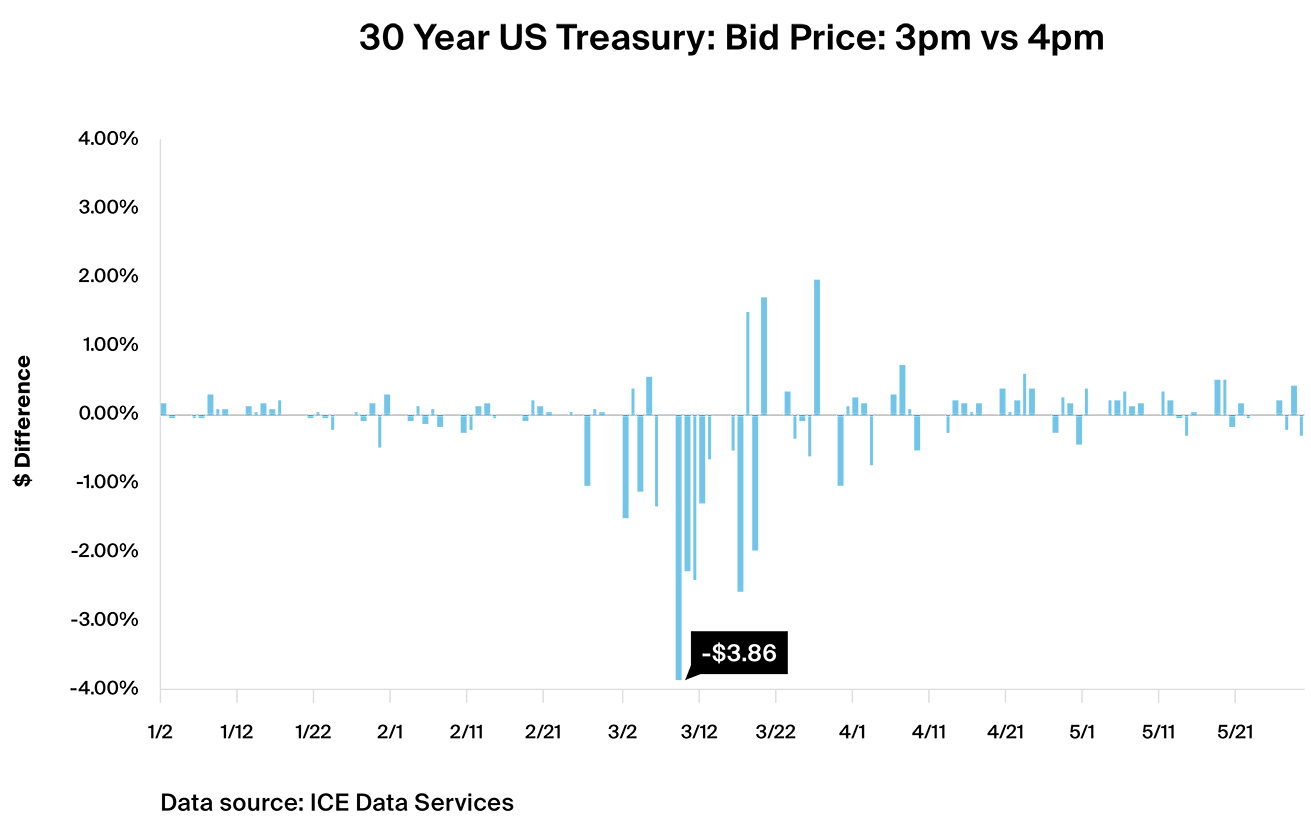

Technical factors also play a role in increased discrepancies. For example, the closing price on the exchange for all US domiciled ETFs is 4pm — but depending on the ETF issuer’s pricing policy, the NAV price may be calculated at 3pm. In calm markets there is minimal difference between the price at 3pm vs 4pm. But in volatile markets, big differences can add to discrepancies between the ETF market price and its net asset value. For instance, the chart below shows the difference between 3pm and 4pm for the on-the-run 30 year US Treasury note from February 2020 to April 2020.

30 Year US Treasury: Bid Price: 3pm vs 4pm

Price uncertainty

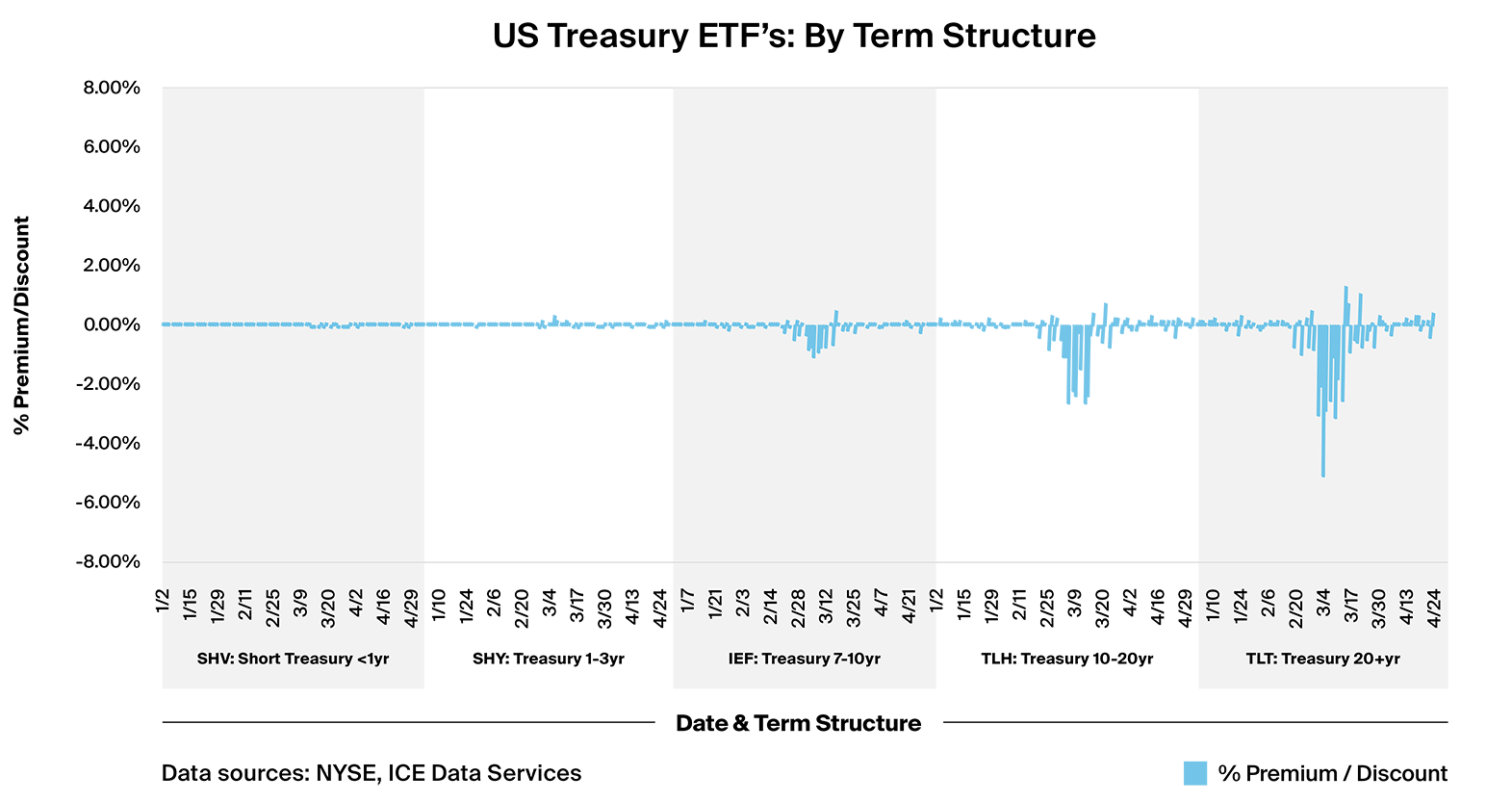

The creation/redemption process that keeps an ETF’s share price reflective of its portfolio value can be affected in rocky markets. Amid the volatility in March, this dislocation was clear across bond ETFs, including US Treasury ETFs. US Treasuries are some of the most liquid fixed income instruments, and usually see higher trading activity in volatile markets. Yet per below, even a 20+ year US Treasury ETF (TLT) traded at a 5% discount in March. Here, the chart shows premiums and discounts across Treasury ETFs with different maturities - with larger dislocation where bonds have a longer maturity.

US Treasury ETFs: By Term Structure

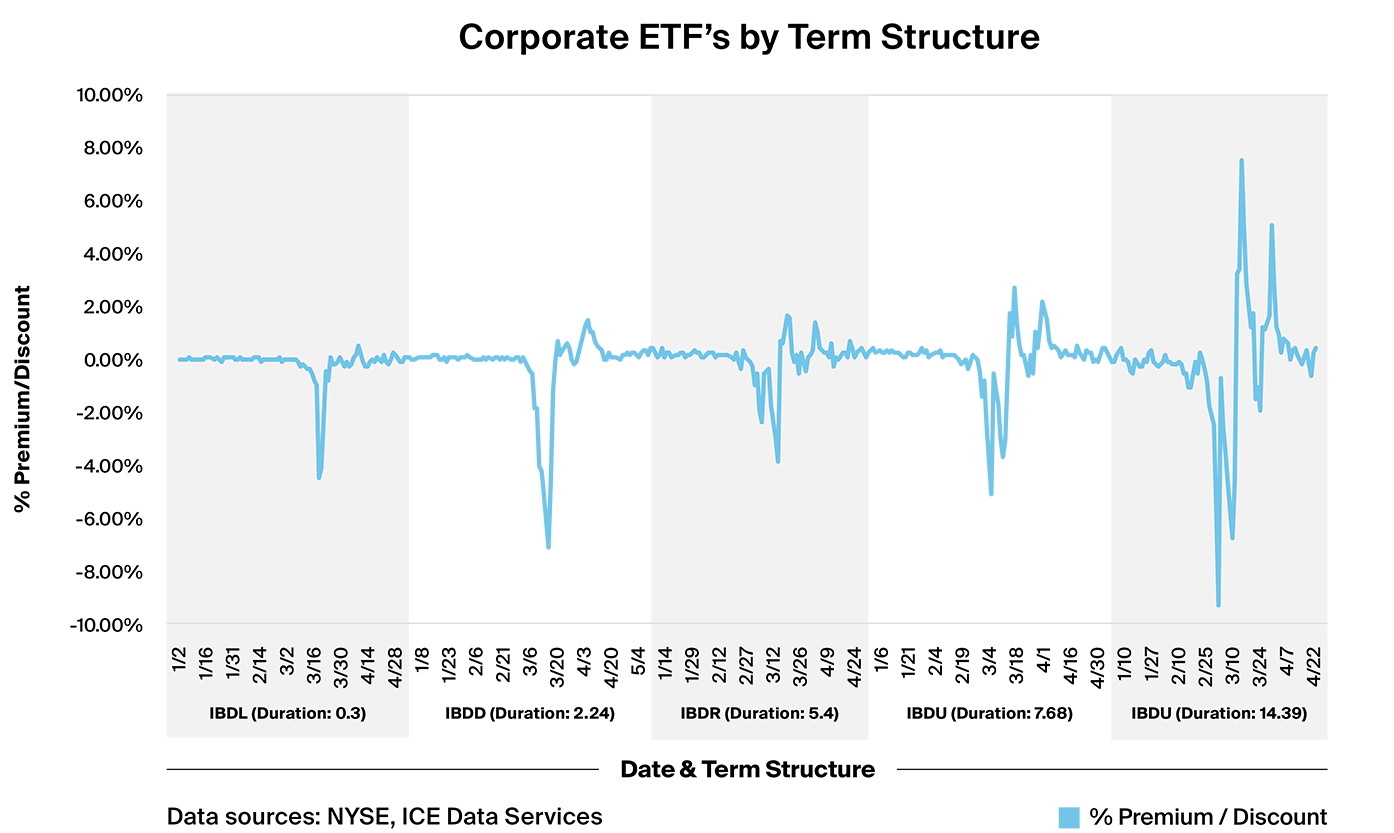

The disconnect was even more stark for corporate bond ETFs. Unlike Treasuries, where the disconnect mainly affected longer dated ETF’s, corporate bond ETF’s saw dislocations regardless of term structure.

Corporate ETF's by Term Structure

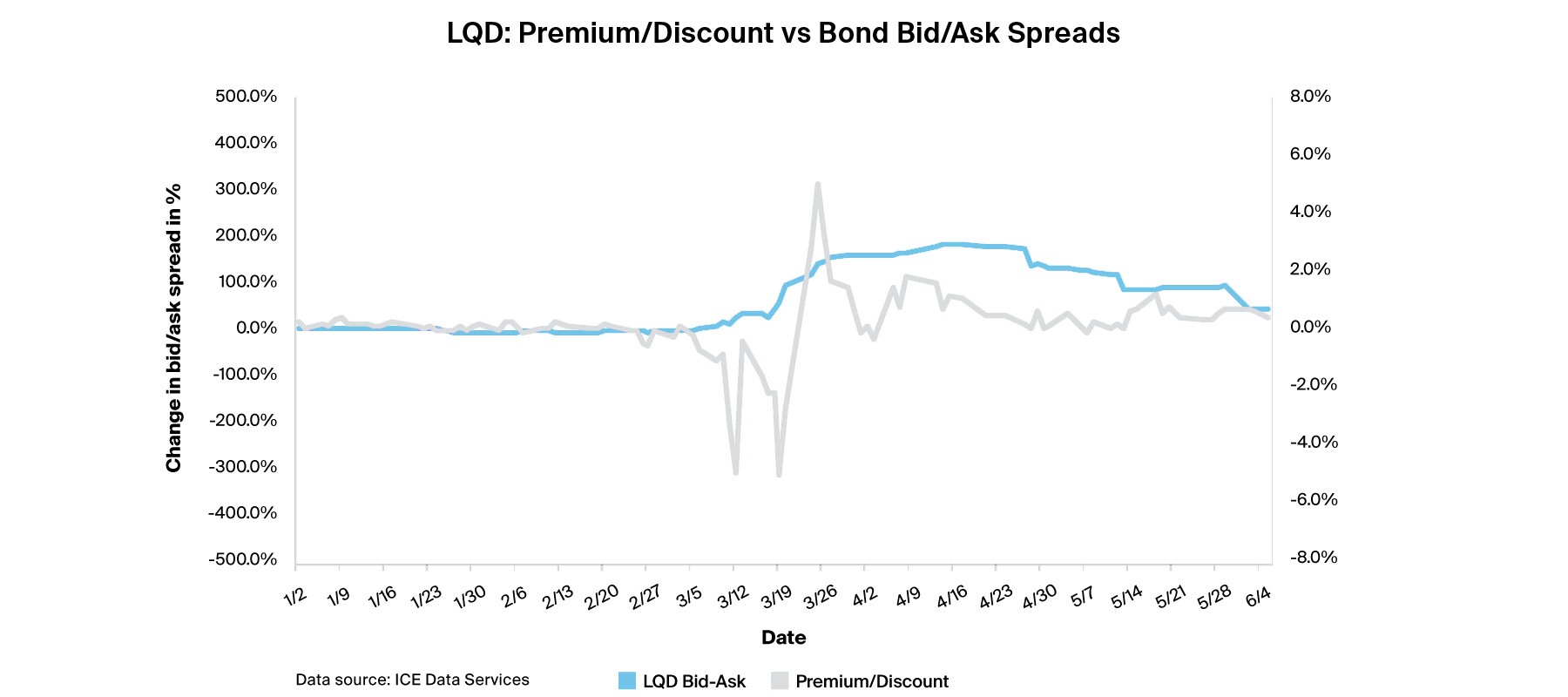

This may in part be attributed to price uncertainty corroborated by a widening of bond bid-ask spreads. The chart below shows the average bid-ask spread for constituent bonds of the corporate bond ETF, LQD vs premium/discounts. The increase in quoted bid-ask spreads reflects market uncertainty and unwillingness to take on risk in the face of this uncertainty.

LQD: Premium/Discount vs Bond Bid/Ask Spreads

We also reviewed trading data on constituent bonds for the corporate bond ETF: LQD. We looked at bonds rated “A” by S&P and animated traded levels from February 2020 to April 2020 in the chart below.

Bonds in LQD that traded > 1mln in size

* We analyzed the trade data reported to TRACE for the consituent bonds for LQD with a credit rating of “A+”, “A” & “A-“ by S&P. We only considered trades above $1 million in size.

The relatively tight yield bands in February show general agreement on credit quality across the term structure. By contrast, March saw yields jump higher across the board and become more disparate, indicating greater ambiguity about credit quality with wider bid/ask spreads reflecting higher execution uncertainty, which caused premium/discount dislocations with the ETF.

In summary, the dislocation between an ETF’s traded price and net asset value is a function of liquidity and transparency. Differences in liquidity across ETFs and the underlying asset classes within the ETF are both factors to consider when evaluating fixed income ETFs. While exchange-traded securities like equities also experience these dislocations, price transparency results in a fast correction. This is not the case in fixed income, where reduced liquidity and more friction in trading reflect a larger, more complex universe of securities. While the fragmented nature of fixed income securities will always drive some disparity, the rise of electronic markets — and their associated speed and transparency benefits — means that the gulf between equity and fixed income ETFs is set to shrink longer term.