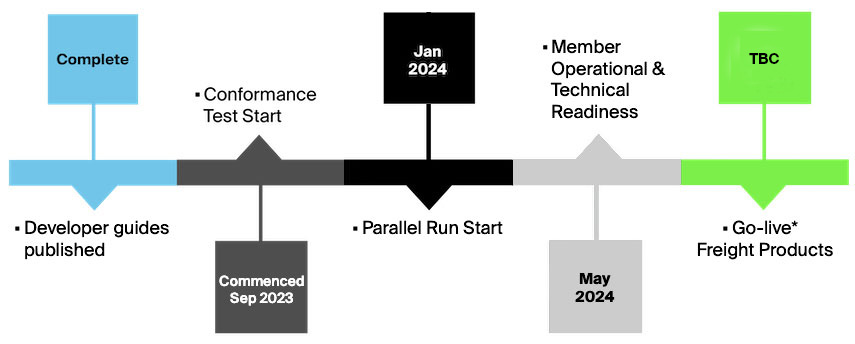

The first group of ICE Clear Europe products to switch to IRM 2 will be Energy Futures and Options. IRM 2 will be rolled out to other product groups in successive stages. Key milestones for the Energy migration are summarized below. Full details are available in the Member Transition Plan

* Go-live of initial product set Freight is subject to completion of all relevant regulatory processes

ICE Equity Index Futures cleared at ICE Clear U.S. went live on January 24, 2022. Rollout of additional products will be implemented in successive stages.